Most Special Purpose Acquisition Companies (SPACs) have failed to meet investors’ expectations. How can regulators address the risks while capturing the potential upside of this novel market structure?

Authored by Martin Szydlowski

In 2021, Special Purpose Acquisition Companies, or SPACs, raised US$162.5 billion. Endorsed by celebrities as wide-ranging as Shaquille O’Neal, Jay-Z, and Paul Ryan, SPACs were touted as a faster, more efficient way for innovative private companies to enter public markets—yet the data has shown that the majority of SPACs have in fact lost money. What can regulators do to ensure that investors and economies actually capture the potential of this new business structure?

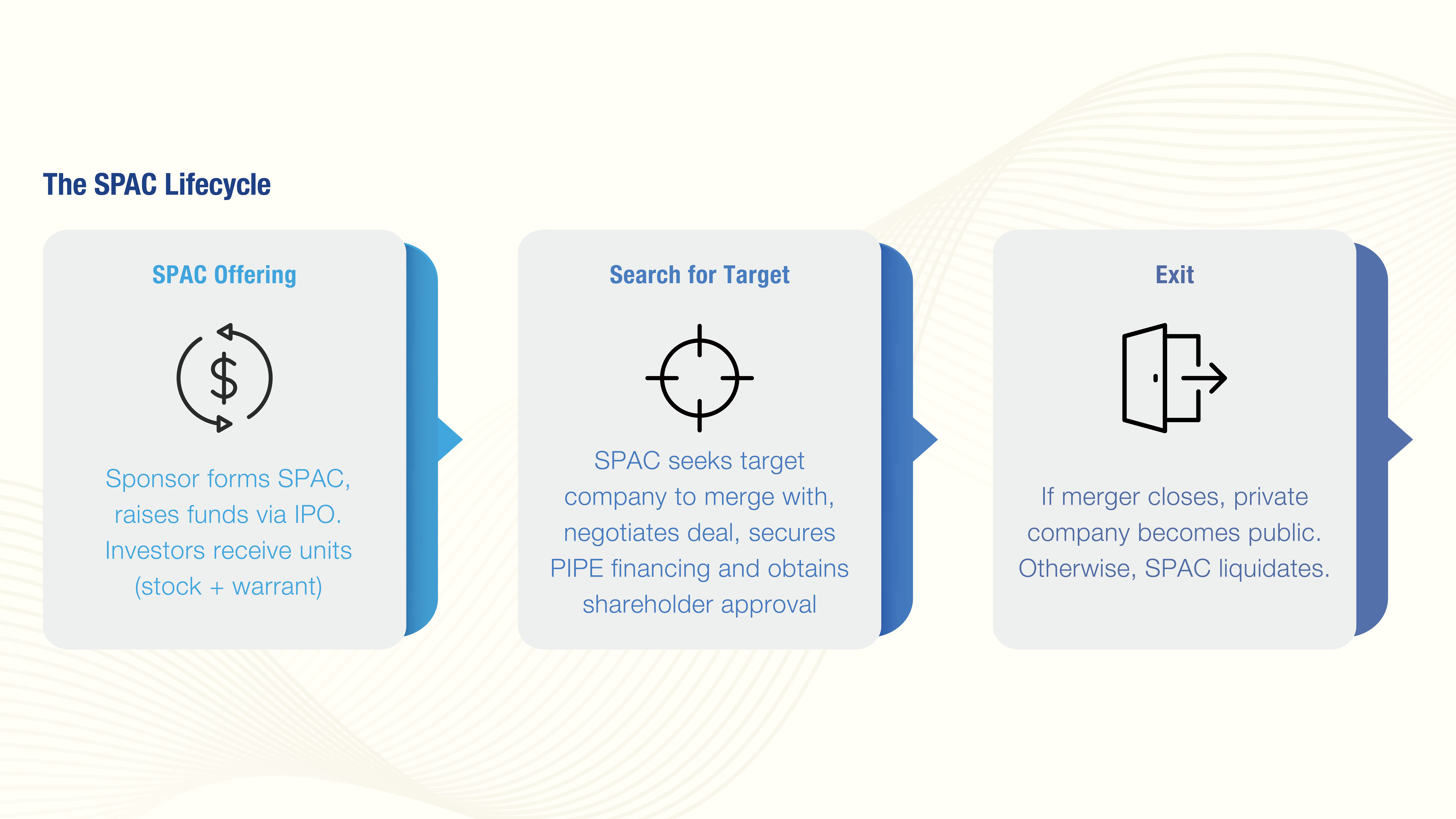

To answer this question, it is critical first to understand what a SPAC is and how it operates. At a high level, a SPAC is a type of shell company that raises money through an IPO with the intention of acquiring a privately held company. Investors are allowed to sell their shares back to the SPAC at any time if they don’t like a proposed acquisition, and shares typically come with warrants that give investors the right to buy future shares at a fixed price.

It seems like a great deal for investors: All the upside of investing in a promising new company, with redemption rights that let them recoup their losses at any time. Nevertheless, a recent study found that while investors who cashed out before a SPAC merger earned annualized returns of nearly 24%, those who held their shares for at least a year post-merger suffered an average loss of over 11%. Another study found that for every US$10 of cash raised, the median SPAC held only US$6.67 by the time it merged with a target company.

Common explanations for this persistent underperformance fall short. Some analysts have blamed SPACs’ lighter disclosure rules, but rational investors would simply demand a steeper discount for that increased risk, rather than accepting negative returns. Others have suggested that the SPAC structure is meant to reward long-term believers over shorter-term players, yet the data shows these are the very investors who lose out.

In reality, my recent research suggests that this effect is largely driven by investor psychology. The unique structure of SPACs, which allows investors to redeem their shares at a future date, may attract overconfident investors, who overpay for SPAC shares and in turn, on average, end up realizing losses.

The sponsor of a SPAC deal is incentivized to close a deal even if doing so is not beneficial for investors, since their large equity stake can only be sold when an acquisition is completed. Early-stage institutional players tend to act rationally, and as a result, they often sell their shares before the merger goes through. But a significant fraction of investors are retail investors: everyday people who might be lured in by hype, a celebrity sponsor, or a compelling story about a “moonshot” target. These investors tend to hold onto their shares for too long, even if the acquisition is unlikely to be profitable.

In my paper, my coauthor and I argue that this behavior is due to a specific form of overconfidence: The redemption right leads investors to think, “If the deal is bad, I’ll be savvy enough to get out.” The warrants seem to only offer extra upside. Yet, when the time comes to make a decision, these investors often fail to act. They are swayed by optimistic projections, they don’t fully grasp how their shares are being diluted, or they just don’t pay close enough attention to dense merger documents to recognize when they would benefit from jumping ship. Instead, they hold on, waiting for a payout that is unlikely to materialize.

This dynamic results in a transfer of profits from retail investors to SPAC sponsors and institutional investors. Overconfident investors essentially overvalue the warrants and redemption options that they are unlikely to use, making them willing to pay more per share than the “fair” rational value. This direct subsidy flows to the sponsor, to the target company (which may get a higher valuation than it deserves), and to the sophisticated investors who profit from redeeming their shares or exercising their warrants.

In the near term, this means that a few sponsors and institutional investors benefit at the cost of a larger group of less-sophisticated investors. But in the longer term, it also drives market distortions which lead to overinvestment in SPACs and many unprofitable acquisitions.

Short-Term Divergence in Returns

By exploiting their redemption options and the overvaluation of warrants, institutional SPAC investors consistently earn positive, low risk returns. Unsophisticated buy-and-hold investors, on the other hand, are left holding diluted shares in companies whose prices were inflated by their own initial overconfidence. When the hype fades and the reality of the business sets in, the share price tends to fall, leading to negative returns.

Long-Term Market Distortions

Beyond the losses sustained by unsophisticated investors, SPACs also end up distorting markets by funding riskier, “moonshot” projects like pre-revenue electric vehicle companies or conceptual tech platforms. This is because SPACs aren’t subject to the same rigorous disclosure requirements as companies pursuing traditional IPOs, meaning that they can present extremely optimistic projections that draw in overconfident investors.

As a result, objectively unprofitable projects end up getting funded instead of ones that are more likely to succeed long-term. The subsidy of overconfident investors means that these acquisitions are likely to pay off for the sponsor and the target, even if they lose money for long-term public shareholders. Conversely, a solid but “boring” company may not attract investment from SPACs because its lack of volatility makes using redemption rights and warrants unattractive.

Proposed Regulatory Approaches May Backfire

In other words, SPACs result in both losses for regular investors and less-efficient allocation of capital, such that less-profitable projects may get funded and more-profitable projects may not. Moreover, many attempts to address these issues through regulation may come with substantial unintended consequences.

1. More disclosure requirements increase information asymmetry.

One of the most common ways in which regulators tend to try to address market distortions is by increasing disclosure requirements. In theory, if investors have more access to information, they should act more rationally. Unfortunately, in the case of SPACs, this may not be the case.

Instead, providing more technical data can actually widen the gap between sophisticated and unsophisticated investors. This is because sophisticated players will use the new data to refine their advantage, while overconfident investors may become even more overconfident, believing that they understand more without actually changing their behavior (since highly technical data can be highly inaccessible to regular investors). In other words, unsophisticated investors experience the downside of more information asymmetry instead of the upside of improved decision-making.

2. Restricting access shrinks the SPAC market without addressing its core problems.

Another common lever that regulators can pull is restricting access to the SPAC market. Banning retail investors from SPACs would likely improve returns for any who remained, as they would face less competition from an overconfident crowd driving up prices. However, this would also reduce profits for sophisticated investors and shrink the entire SPAC market, potentially closing off a viable (if flawed) path to public markets for some companies.

3. Eliminating key features of SPACs also eliminates their upside.

Similarly, some regulators have proposed eliminating the warrants or redemption rights that make SPACs unique. Removing warrants would remove some of the advantages of this market and make shares less attractive, thereby reducing the potential for overpricing. This would directly benefit buy-and-hold investors, but it would also make it harder for sponsors to fund their ventures. Along the same lines, eliminating redemption rights would turn SPACs into traditional blind-pool investments, forcing all investors to commit their capital for the long term. This would also remove the very feature that overconfident investors overvalue, again shrinking the market.

A Better Way to Tackle the Overconfidence Problem: The SPAC Nutrition Label

My research suggests that a core problem with SPACs is the overconfidence of unsophisticated investors. As such, disclosure requirements mandating hundreds of pages of technical jargon, or market controls that eliminate the very features that make SPACs unique, may not be the best approach.

Instead, a simple, one-page “SPAC Nutrition Label” at the front of every prospectus could help address information asymmetries and reduce investor overconfidence without eliminating SPACs’ potential to fill an important market gap. Like the summary of nutrition facts displayed on food packages, a SPAC Nutrition Label would state, in plain language:

• The percentage of shares held by the sponsor

• The total number of warrants outstanding

• The amount of cash per share remaining after estimated redemptions

• A clear, historical comparison of average SPAC returns versus the S&P 500

This would not prohibit regular investors from investing in SPACs, but it would empower them to make more informed choices when they do so. It would make the true risks more salient, helping to bridge the gap between the perceived and actual value of a SPAC share. As a result, investors would act less overconfidently, ultimately ensuring that capital is allocated toward more-profitable projects and that sponsors and sophisticated investors are not benefiting at the cost of retail investors.

Since their boom in 2021, the SPAC market has shrunken substantially, and the relative attractiveness of the SPAC structure has fallen compared to a traditional IPO. That said, in 2024, SPACs still raised nearly US$10 billion. While SPACs are less popular than they were a few years ago, they are still an important component of the financial ecosystem. As such, it’s critical for regulators to take a clear-eyed approach to capturing their potential while minimizing the risks they pose to regular investors and the economy at large.

Martin Szydlowski is an associate professor of economics at HKUST, focusing on game theory, industrial organization, and finance.

This article draws on the research paper “Harnessing the Overconfidence of the Crowd: A Theory of SPACs,” authored by Snehal BANERJEE and Martin SZYDLOWSKI.